The Hidden Cost of Hospital Consolidation

Hospital consolidation isn’t lowering costs; it’s driving them up. Hospital systems are rapidly acquiring physician practices, and the data is clear on the consequences:

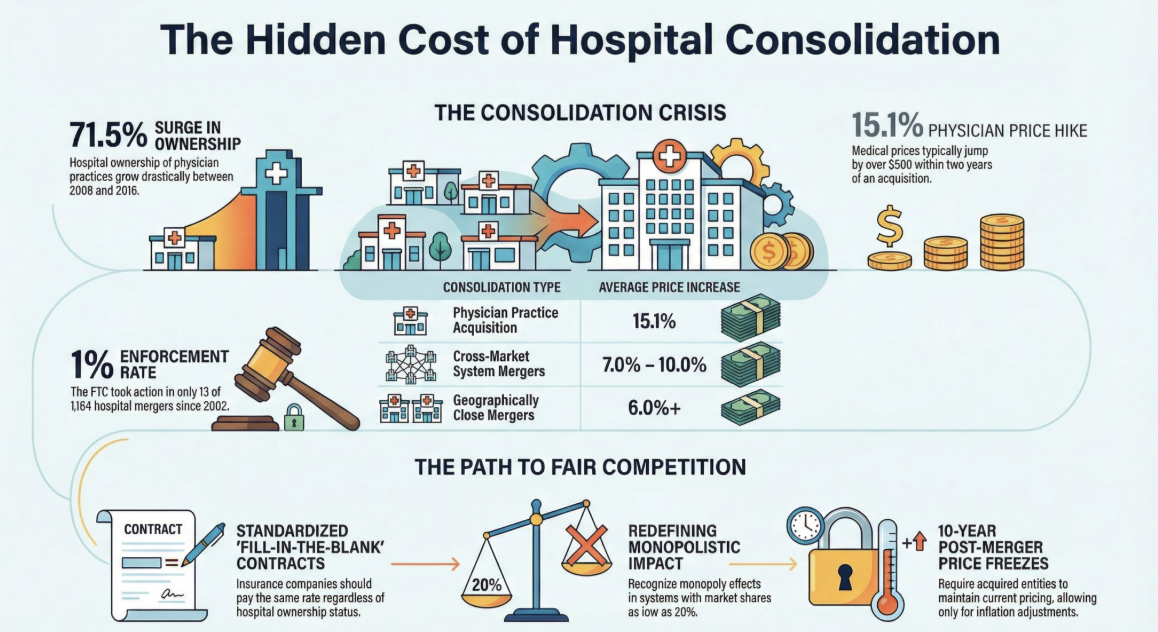

Hospital ownership of physician practices rose 71.5% between 2008 and 2016.

Within two years of acquisition, physician prices increase by 15.1% (≈+$502).

For certain procedures, such as labor and delivery, hospital prices increase by an average of $475 (≈+3.3%) after a practice is acquired.

These deals are largely invisible to federal review: an estimated 99.9% fall below Hart–Scott–Rodino (HSR) reporting thresholds.

Additionally, hospitals are consolidating at an alarming rate. The data is clear what happens after a large health system acquires another hospital:

Prices rise after hospital mergers, especially when hospitals are close substitutes. In one landmark national study of 2007-2011 M&A, prices increased by 6%+ when the merging hospitals were geographically close.

Across a large set of mergers (2009-2016), average commercial price effects are still material, ~5% on average.

Cross-market “system building” mergers can raise prices too: prior research cited in peer-reviewed work finds ~7-10% price increases in certain in-state cross-market acquisitions.

Quality improvements are not reliably observed: major reviews and empirical work generally find price increases without consistent improvement in quality.

Enforcement has been limited relative to deal volume: from 2002-2020 there were 1,164 acute-care hospital mergers and the FTC took action in only 13 (~1%).

The result is a system where scale is rewarded, competition is squeezed out, and patients pay more, without corresponding improvements in access, quality, or outcomes.

The path forward is straightforward:

End financial incentives that favor consolidation by standardizing contracts that insurance companies offer hospitals. Every contract offered to every hospital should have minimal variance and should simply take a “fill in the blank” approach. Care paid the same regardless of ownership.

Apply real scrutiny to mergers that reduce competition, especially when rivals lose access to physicians.

The FTC needs to get real about anti-trust. A health system can enjoy the effects of a monopoly without controlling a majority of the market. Even a market share as small as 20% can create a monopolistic impact when services like OB, ICU and emergency room services are included.

Allow physicians to own hospitals.

If a hospital does get past FTC scrutiny and is allowed to proceed with the acquisition require them to retain current pricing for a period of 5-10 years with only CPI increases.

Healthcare works best when competition is real, incentives are aligned, and consumers, not systems, are at the center of the market.

Sources: Yale Tobin Center for Economic Policy; National Bureau of Economic Research (NBER); Health Affairs; Federal Trade Commission (FTC).